10 Best Life Insurance Companies That Won’t Increase Rates in 2026 (Find the Top Providers Here)

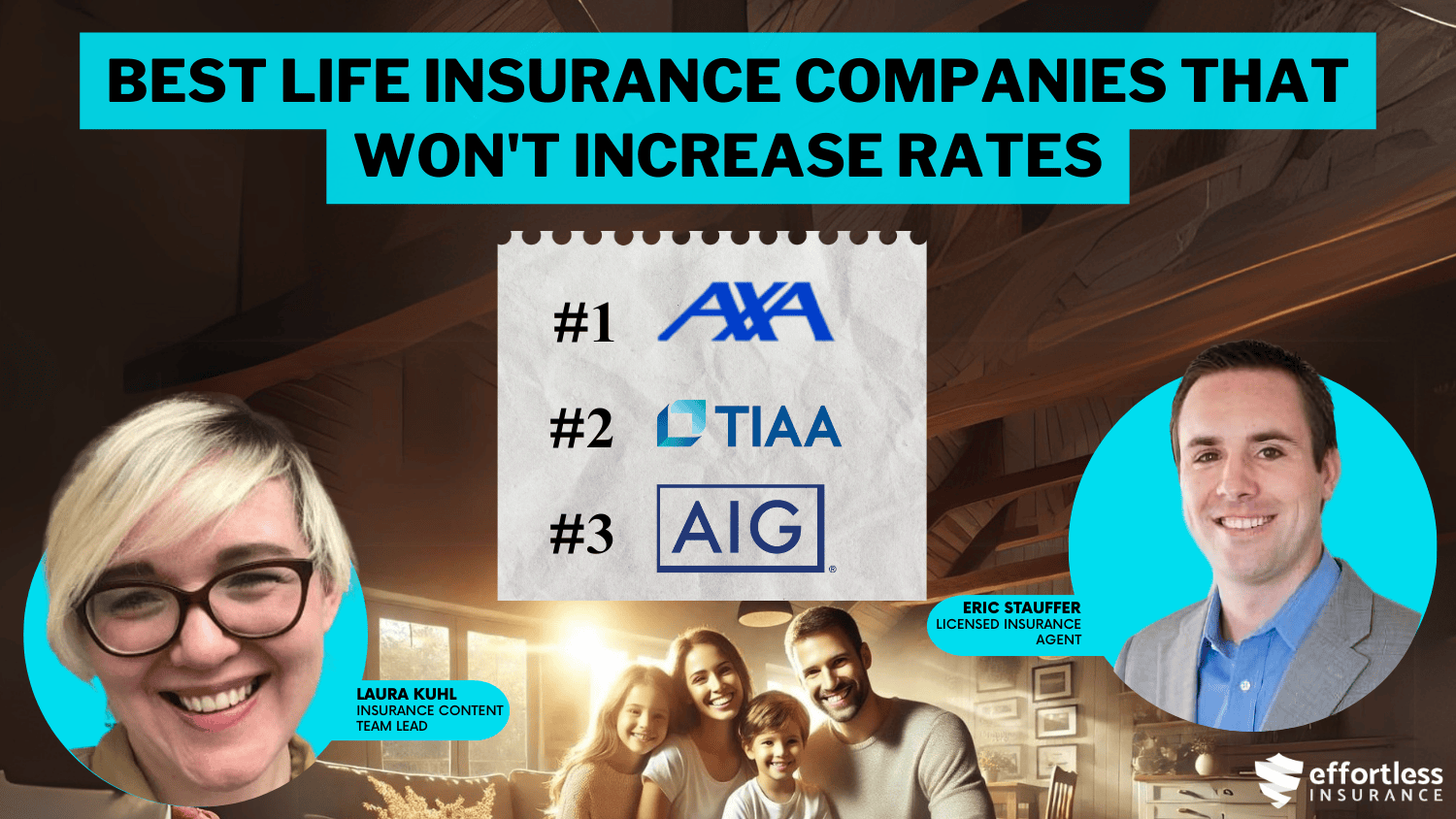

The best life insurance companies that won't increase rates are AXA, TIAA, and AIG, starting at only $38 per month. These companies guarantee long-term financial security for policyholders, commit to providing affordable, consistent coverage, and offer rates that won't increase.

Free Life Insurance Comparison

Compare Quotes From Top Companies and Save

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Eric Stauffer

Licensed Insurance Agent

Eric Stauffer is an insurance agent and banker-turned-consumer advocate. His priority is educating individuals and families about the different types of insurance coverage. He is passionate about helping consumers find the best coverage for their budgets and personal needs. Eric is the CEO of C Street Media, a full-service marketing firm and the co-founder of ProperCents.com, a financial educat...

Licensed Insurance Agent

UPDATED: Aug 24, 2025

It’s all about you. We want to help you make the right coverage choices.

Advertiser Disclosure: We strive to help you make confident life insurance decisions. Comparison shopping should be easy. We are not affiliated with any one life insurance provider and cannot guarantee quotes from any single provider. Our life insurance industry partnerships don’t influence our content. Our opinions are our own. To compare quotes from many different companies please enter your ZIP code on this page to use the free quote tool. The more quotes you compare, the more chances to save.

Editorial Guidelines: We are a free online resource for anyone interested in learning more about life insurance. Our goal is to be an objective, third-party resource for everything life insurance related. We update our site regularly, and all content is reviewed by life insurance experts.

UPDATED: Aug 24, 2025

It’s all about you. We want to help you make the right coverage choices.

Advertiser Disclosure: We strive to help you make confident life insurance decisions. Comparison shopping should be easy. We are not affiliated with any one life insurance provider and cannot guarantee quotes from any single provider. Our life insurance industry partnerships don’t influence our content. Our opinions are our own. To compare quotes from many different companies please enter your ZIP code on this page to use the free quote tool. The more quotes you compare, the more chances to save.

On This Page

163 reviews

163 reviewsCompany Facts

Whole Policy for No Rate Increases

A.M. Best

Complaint Level

163 reviewsThe best life insurance companies that won’t increase rates are AXA, TIAA, and AIG, offering reliable coverage with rates starting at $38 per month.

AXA stands out as the top pick for its balance of affordability, strong financial ratings, and consistent premium guarantees. For more information, review the best life insurance companies here.

Our Top 10 Company Picks: Best Life Insurance Companies That Won't Increase Rates

| Insurance Company | Rank | Bundling Discount | A.M. Best | Best For | Jump to Pros/Cons |

|---|---|---|---|---|---|

| #1 | 15% | A | Financial Stability | AXA | |

| #2 | 10% | A++ | Retirement Plan | TIAA |

| #3 | 12% | A | High Coverage | AIG | |

| #4 | 10% | A+ | Affordable Plans | Transamerica | |

| #5 | 25% | A | Comprehensive Plan | Liberty Mutual | |

| #6 | 10% | A | No Exam | Lincoln Financial | |

| #7 | 10% | A++ | Financial Strength | MassMutual | |

| #8 | 15% | A++ | Dividend Policies | Northwestern Mutual | |

| #9 | 10% | A++ | Policy Customization | Guardian Life | |

| #10 | 10% | A+ | Customer Service | Mutual of Omaha |

TIAA and AIG are well-known and offer good rates with choices that fit different needs. These providers ensure long-term stability, making them ideal for anyone seeking dependable life insurance.

Simplify your life insurance shopping by entering your ZIP code into our free quote comparison tool and find coverage that fits your budget and needs.

- AXA stands out as the best life insurance company that won’t increase rates

- AXA, TIAA, and AIG offer tailored policies that won’t increase rates over time

- All three companies offer affordable premiums, starting at $38 per month

#1 – AXA: Top Overall Pick

Compare Quotes From Top Companies and Save

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Pros

- Financial Stability: AXA has an “A” rating from A.M. Best, showing they are financially stable and won’t increase rates. Check this AXA Life Insurance Company Review for more info.

- Affordable Rates: AXA offers competitive rates starting at $50/month for term life insurance and $150/month for whole life insurance that won’t increase over time.

- Bundling Discounts: Get a 15% discount when you bundle life insurance with other policies, offering steady savings you can count on that won’t increase rates.

Cons

- Limited Policy Customization: AXA may not offer as many customization options for term policies, which could affect tailored coverage over time.

- Higher Whole Life Costs: Whole life premiums are competitive, but rate increases over time may be slightly higher compared to other providers.

#2 – TIAA: Best for Retirement Plan

Pros

- Retirement Plan: TIAA offers life insurance with retirement plans, starting at $41/month for term life and $133/month for the whole life, which won’t increase the rates.

- Stable Premiums: With an “A++” A.M. Best rating, TIAA ensures predictable rates that won’t increase unexpectedly. Check this TIAA Life Insurance Review to learn more.

- Affordable Bundling: TIAA offers a 10% discount when you bundle, providing consistent savings that will not increase rates over time.

Cons

- Lower Bundling Discount: The bundling discount is less generous than some competitors, which could affect cumulative savings, but rates won’t increase.

- Limited Coverage Options: High coverage limits may require additional underwriting, which could affect future adjustments, but rates won’t increase.

Compare Quotes From Top Companies and Save

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

#3 – AIG: Best for High Coverage

Pros

- High Coverage Limits: AIG provides high coverage options with rates starting at $52/month for term life insurance and $160/month for whole life insurance that won’t increase.

- Stable Rates: AIG’s “A” A.M. Best rating ensures consistent pricing that won’t increase with market conditions. For more details, check this AIG Life Insurance Review.

- Bundling Benefits: A 12% discount when bundling keeps your savings steady, meaning your rates won’t increase for multiple policies.

Cons

- Rate Guarantees Limited: AIG offers stable rates, but some policies might not have the same long-term guarantees, which could concern those looking for lifelong price protection.

- Whole Life Premiums: Whole life rates may be slightly higher compared to competitors, though they remain stable over time.

#4 – Transamerica: Best for Affordable Plans

Compare Quotes From Top Companies and Save

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Pros

- Affordable Pricing: Transamerica offers rates starting at $40/month for term life and $125/month for whole life insurance that won’t increase over time.

- Strong Financial Standing: With an “A+” rating, Transamerica provides a reliable foundation for steady premiums that won’t increase.

- Consistent Bundling: A 10% discount for bundling helps you save regularly, and the rates won’t increase. Read this Transamerica Life Insurance Company Review for more details.

Cons

- Limited Features: Transamerica might not have as many options as some other providers, which could make it harder to adjust if rates increase.

- Smaller Discounts: The bundling discount is lower than some competitors, impacting cumulative savings over time and ensuring rates won’t increase significantly.

#5 – Liberty Mutual: Best for Comprehensive Plan

Pros

- Comprehensive Plans: Liberty Mutual provides a variety of insurance options with rates starting at $48/month for term life and $140/month for whole life insurance, which won’t increase over time.

- Competitive Rates: Fixed premiums mean policyholders won’t face surprise rate increases. Find out more in this Liberty Mutual Life Insurance Review.

- Significant Savings: By bundling insurance policies, policyholders can save 25% on their rates, ensuring additional savings over time.

Cons

- More Complexity: Comprehensive plans may require more attention, but managing them won’t increase rates unpredictably.

- Slightly Higher Premiums: Term life insurance premiums are competitive, and while slightly higher, they won’t increase beyond a steady level.

Compare Quotes From Top Companies and Save

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

#6 – Lincoln Financial: Best for No Exam

Pros

- No Exam Requirement: Lincoln Financial provides quick coverage with rates starting at $42/month for term life insurance and $135/month for whole life insurance that won’t increase.

- Flexible Coverage: Lincoln Financials’ variety of riders ensures customizable, stable coverage options at rates that won’t increase.

- Stable Premiums: Lincoln Financial rates are affordable, ensuring no unexpected rate increases in the future. Read more: No Exam Life Insurance

Cons

- Limited Availability: Coverage might be limited in some states, reducing long-term flexibility and making it harder to guarantee that rates won’t increase.

- Moderate Financial Strength: Lincoln’s “A” rating from A.M. Best is reliable but slightly lower, which could affect premium stability and guarantee that rates won’t increase in the future.

#7 – MassMutual: Best for Financial Strength

Compare Quotes From Top Companies and Save

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Pros

- Financial Stability: MassMutual’s “A++” A.M. Best rating ensures that term life insurance rates, starting at $54/month, will remain steady and won’t increase over time.

- High Coverage Limits: They offer affordable premiums with high coverage limits, ensuring lasting protection without rate increases.

- Strong Customer Support: Great service means everything runs smoothly, and your policy stays the same without unexpected rate increases.

Cons

- Higher Premiums: Whole life insurance rates are slightly higher, though they remain stable and won’t increase over time.

- Read more: What is face value in life insurance?

- Limited Online Tools: Though online tools are easy to use, they might not have the advanced features for policy management.

#8 – Northwestern Mutual: Best for Dividend Policies

Pros

- Stable Rates: Northwestern Mutual offers stable life insurance rates at $49/month for term life and $152/month for whole life, with no rate increases.

- High Customization: Customizing your policy often means your rates won’t increase as needs evolve. Get more details by reading this Northwestern Mutual Life Insurance Review.

- Strong Financial Strength: An “A++” A.M. Best rating means the company is very reliable and offers steady pricing, which means they are unlikely to increase rates unexpectedly.

Cons

- Long Application Process: The application might require more paperwork, which could take longer to make quick changes.

- Limited Digital Experience: Online services might not be as advanced as others, which could slow down real-time updates.

Compare Quotes From Top Companies and Save

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

#9 – Guardian Life: Best for Policy Customization

Pros

- Policy Customization: The Guardian offers tailored coverage with rates starting at $38/month for term life insurance and $115/month for whole life insurance.

- Stable Premiums: With an “A++” A.M. Best rating, the Guardian rates are steady, meaning they won’t increase unpredictably.

- Competitive Pricing: Low prices make it easier to save money and stay on budget, with no surprise rate increases to worry about.

Cons

- Limited Coverage Options: Fancy extras might cost more or have special rules, but they usually won’t make your rates go up out of the blue.

- Changing Premiums Over Time: Prices might change a bit, but they usually won’t increase significantly, keeping your budget steady. Read more: What does life insurance cover?

#10 – Mutual of Omaha: Best for Customer Service

Pros

- Exceptional Service: Mutual of Omaha ensures a smooth handling of life insurance with rates starting at $45/month for term life and $130/month for whole life insurance.

- Affordable Premiums: Low, steady premiums give you reliable coverage, so you don’t have to worry about sudden rate increases.

- High Policy Flexibility: Mutual of Omaha policies offer different add-on options while keeping your costs the same over time. Visit this Mutual of Omaha Life Insurance Review for more info.

Cons

- Moderate Financial Rating: Though an “A+” rating is stable, it’s just a notch below the best providers. But that doesn’t impact your rates.

- Limited Digital Features: Online tools might not be as sophisticated, but that doesn’t affect the fact that your rates will stay the same.

Compare Quotes From Top Companies and Save

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Finding the Right Life Insurance for Your Needs and Budget

Choosing the right life insurance policy can feel daunting, with many companies, options, and varying rates influenced by factors like age and gender. Understanding these differences is key to finding a policy that fits your needs and budget.

Term and Whole Life Rates From Companies That Won't Increase Monthly Rates

| Insurance Company | Term Policy | Whole Policy |

|---|---|---|

| $52 | $160 | |

| $50 | $150 | |

| $38 | $115 | |

| $48 | $140 | |

| $42 | $135 | |

| $54 | $155 | |

| $45 | $130 | |

| $49 | $152 | |

| $41 | $133 |

| $40 | $125 |

The three main types of life insurance are term life, whole life, and universal life, with universal life offering additional subcategories. Each policy type provides distinct advantages, so it’s important to match your choice with your financial goals and priorities.

Life insurance companies that won’t increase rates provide reliable coverage and protect you from unexpected premium hikes.

Tim Bain Licensed Insurance Agent

Term life insurance features level premiums, but only for the policy’s term, e.g., 30 years. After that, rates can increase if you renew. For lifelong stability, whole life and universal life policies offer fixed premiums that never change, making them ideal for long-term predictability.

Understanding Term and Whole Life Insurance Options

Choosing the best whole life insurance company depends on your specific needs and policy details. Factors such as coverage amount, budget, and long-term goals play a significant role in making the right choice. Asking important questions, such as how much coverage you need, the costs involved, and the independence of your beneficiaries, is crucial to finding the best fit.

It’s Life Insurance Awareness Month! The benefits of life insurance can help anyone at any age prepare for the unexpected. This month is a good time to reflect and celebrate life insurance and its role in helping secure your family’s financial future and peace of mind. pic.twitter.com/ogxj1SSZ58

— Transamerica (@Transamerica) September 3, 2024

Choosing the top term life insurance companies and comparing term life insurance rates are essential tools for finding the best fit. Adding considerations such as the best rates for life insurance ensures that individuals receive affordable premiums while maintaining quality coverage.

Term life insurance rate comparison helps individuals find the most cost-effective policies tailored to their specific coverage needs. Additionally, comparing life insurance rates and life insurance companies’ ratings ensures a thorough evaluation of the offerings.

For many, the best life insurance company offers the most affordable rates for the desired coverage. However, comparing term life insurance to whole life insurance can be complex. Comparing life insurance companies’ ratings allows consumers to assess insurer reliability and customer satisfaction.

Read more: Term vs. Permanent Life Insurance: Which is better?

Term life insurance is generally more budget-friendly, while whole life insurance provides lifetime coverage at a higher cost. For example, a 60-year-old might pay around $100 per month for term life, compared to over $700 for whole life insurance. Additionally, State Farm’s best whole-life insurance policy offers long-term financial security with a cash value component.

If there’s a good chance you’ll outlive a term policy, it may be a better choice, as its rates stay the same. Additionally, for those on a budget, universal life insurance offers more flexibility in premium adjustments compared to whole life insurance. Balancing affordability, stability, and coverage is key to finding the best option.

Choosing the Right Life Insurance Policy With Stable Rates

Life insurance reviews offer insight into policy features, benefits, and potential drawbacks. Additionally, selecting the best life insurance policy with level premiums requires thorough research into ratings, reviews, and costs. Our life insurance underwriting guide can help simplify this process.

Discounts From the Top Life Insurance Companies That Won't Increase Rates

| Insurance Company | Available Discounts |

|---|---|

| Bundling, Wellness Savings, Annual Payment, Non-Smoker, Healthy Living | |

| Bundling, Health Discount, Annual Payment, Non-Smoker, Safe Lifestyle | |

| Bundling, Health Discount, Annual Payment, Safe Living, Loyalty Reward | |

| Bundling, Annual Payment, Healthy Lifestyle, Home Safety, Vehicle Safety | |

| Group Rates, Wellness Discount, Non-Smoker, Annual Payment, Safe Lifestyle | |

| Annual Payment, Health Discount, Loyalty Reward, Bundling, Group Rates | |

| Annual Payment, Wellness Savings, Non-Smoker, Healthy Living, Loyalty Discount | |

| Non-Smoker, Annual Payment, Group Rates, Healthy Lifestyle, Loyalty Discount | |

| Bundling Discount, Annual Payment, Health Savings, Group Rates, Loyalty Reward |

| Group Rates, Non-Smoker, Annual Payment, Loyalty Discount, Safe Activities |

Start by comparing life insurance quotes from different insurers to find options that fit your budget. Keep in mind that the cheapest life insurance for men or seniors may vary based on individual needs. It’s important to evaluate not only the cost but also the coverage to ensure it meets your long-term financial goals.

To make a more informed decision, check company ratings and Better Business Bureau accreditation to ensure a strong history of customer satisfaction and complaint resolution. Additionally, look for policies that offer additional benefits, such as riders for critical illness or accidental death, to provide a more comprehensive level of protection.

Consider the financial strength of the insurer by reviewing their credit ratings from agencies like AM Best or Standard & Poor’s. This helps ensure the company can meet its future obligations and provides peace of mind in case of unforeseen events.

Choosing a life insurance company that won't increase rates ensures your premiums remain predictable and affordable, offering peace of mind and financial security over time.

Daniel Walker Licensed Insurance Agent

Furthermore, understanding the insurer’s claims process can provide insight into how smoothly they handle payouts and support policyholders in times of need.

Compare Quotes From Top Companies and Save

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Case Studies: Real Stories of Individuals Who Found Life Insurance With no Rate Increase

These stories show how important it is to have steady, personalized coverage to keep your financial future safe. For more information on the types of life insurance, click here.

Case Study #1: AXA’s Long-Term Stability

John and Sarah chose AXA for their life insurance because they liked that their premiums stayed the same at $50 per month.

Case Study #2: TIAA’s Personalized Coverage

Maria chose TIAA’s flexible policies because they worked well for her family. The coverage was steady, with no unexpected changes.

Case Study #3: AIG Reliable Coverage

James chose AIG because of its strong financial stability. He felt secure knowing that AIG offers steady premiums, ensuring reliable coverage for many years.

These examples show how AXA, TIAA, and AIG providers offer steady, dependable life insurance plans that fit personal needs and give lasting financial peace of mind. Additionally, the top 20 life insurance companies provide a wide range of options for consumers looking for reliable and trusted providers.

Choosing Life Insurance Companies That Won’t Increase Rates

Comparing life insurance companies helps you find reliable providers that offer consistent rates without unexpected increases. These plans give you peace of mind by staying affordable and protecting your family over time.

Read more: Where To Buy Life Insurance

When looking for a plan, choose companies with good ratings and transparent rules. With the right company, you can get coverage that fits your needs and keeps your future safe. Additionally, consider State Farm as one of the top life insurance companies, known for offering reliable coverage without unexpected rate increases. If you want to explore your life insurance options, enter your ZIP code in our free tool to get started.

Frequently Asked Questions

Why is a strong financial rating important?

A high financial rating indicates the company’s ability to meet future claims without raising rates. By comparing life insurance companies, you can evaluate life insurance’s best rates and find the most suitable coverage. For example, the best State Farm life insurance policy offers a range of choices between State Farm’s whole life insurance vs term.

Can I customize my policy with these providers?

Yes, AXA, TIAA, and AIG offer flexible options that allow you to adjust coverage while maintaining stable rates. Enter your ZIP code into our free comparison tool to explore affordable life insurance rates today.

What makes the best life insurance companies unique?

The best life insurance companies that won’t increase rates provide stable, consistent premiums and reliable coverage for the long term. Additionally, when searching for the best life insurance rates, it’s important to consider various options like top life insurance companies and top-rated life insurance providers. Find out how life insurance works.

How often do these companies review premiums?

Premium reviews are conducted regularly, usually annually, to ensure rates stay fair and consistent. Term life insurance companies assess premiums to reflect changes in risk and market conditions. Comparing term life insurance rates and evaluating companies’ ratings helps individuals make informed choices for the best coverage.

What happens during policy renewals?

Policy renewals with these companies ensure ongoing coverage without unexpected rate hikes. Additionally, State Farm’s best whole-life insurance policy combines protection with savings for a stable financial future.

How do AXA, TIAA, and AIG maintain steady premiums?

These companies use comprehensive risk management and tailored strategies to ensure premiums stay predictable and fair. Check out the dos and don’ts of life insurance for added info.

Can I switch insurers if needed?

Yes, you can switch between top life insurance companies, though medical underwriting may be required. Furthermore, life insurance companies’ ratings provide insights into their financial stability and customer satisfaction while comparing term life insurance rates helps understand which option is more affordable.

Do they offer family or joint policies?

Yes, AXA, TIAA, and AIG provide family and joint coverage with steady premiums. Additionally, they offer the best life insurance for seniors, and State Farm provides tailored policies that meet the unique needs of older individuals, ensuring peace of mind. The State Farm term life insurance quotes simplify the process by offering transparent pricing and policy options.

Are individuals with pre-existing conditions covered?

Yes, AXA, TIAA, and AIG provide coverage for individuals with pre-existing conditions while maintaining stable premiums. For more details, discover how a pre-existing condition affects life insurance.

How do they prevent premium increases?

These companies offer plans designed to lock in rates and avoid unexpected increases. Enter your ZIP code into our free quote comparison tool to instantly compare life insurance quotes from trusted insurers near you.

Compare Quotes From Top Companies and Save

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Eric Stauffer

Licensed Insurance Agent

Eric Stauffer is an insurance agent and banker-turned-consumer advocate. His priority is educating individuals and families about the different types of insurance coverage. He is passionate about helping consumers find the best coverage for their budgets and personal needs. Eric is the CEO of C Street Media, a full-service marketing firm and the co-founder of ProperCents.com, a financial educat...

Licensed Insurance Agent

Editorial Guidelines: We are a free online resource for anyone interested in learning more about life insurance. Our goal is to be an objective, third-party resource for everything life insurance related. We update our site regularly, and all content is reviewed by life insurance experts.